What Is ASB 2? Dividend History, Pros, Cons & Investment Strategies

What Is ASB 2?

ASB 2, or its full name Amanah Saham Bumiputera 2, is a fixed-price unit trust fund managed by Amanah Saham Nasional Berhad (ASNB), a subsidiary of Permodalan Nasional Berhad (PNB). The fund was launched on 19 March 2014 as a complement to the original ASB fund that has long been a favorite among Bumiputera investors.

In short, ASB 2 gives Bumiputera investors the opportunity to invest an additional RM300,000 - on top of the existing RM300,000 limit for the original ASB. This means your combined investment in both ASB and ASB 2 can reach up to RM600,000.

Just like ASB, each unit of ASB 2 is fixed at RM1.00. Your capital is preserved, and you do not need to worry about unit price fluctuations like other variable-price unit trust funds.

Why Was ASB 2 Established?

Before 2014, many Bumiputera investors had already reached the maximum limit of RM200,000 (later raised to RM300,000) in their ASB accounts. They wanted to continue investing within the ASNB ecosystem but had no room left.

PNB established ASB 2 to solve this problem. With ASB 2, investors who have already "maxed out" their ASB can continue investing in ASNB's fixed-price funds without having to switch to variable-price funds like ASN or ASM.

Since its launch, ASB 2 has attracted over 614,000 unit holders with total units in circulation exceeding 14.12 billion units as of FY2025.

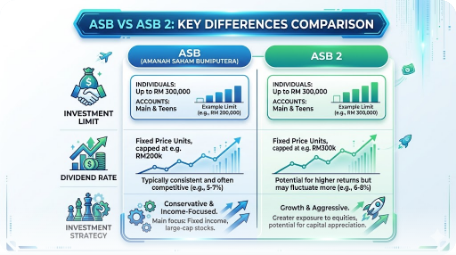

Differences Between ASB and ASB 2

Many people confuse ASB and ASB 2. Although both are managed by ASNB with a fixed price of RM1.00, there are several important differences:

Investment Strategy

ASB focuses its investments primarily in equities (stocks) for long-term growth. ASB 2, on the other hand, uses a mixed-asset strategy - a combination of equities and fixed-income securities (bonds). This makes ASB 2 slightly more conservative compared to ASB.

Investment Limits

| Feature | ASB | ASB 2 |

|---|---|---|

| Maximum limit | 300,000 units (RM300k) | 300,000 units (RM300k) |

| Unit price | RM1.00 (fixed) | RM1.00 (fixed) |

| Financial year | January - December | April - March |

| Strategy | Equity-focused | Mixed-asset |

| Management fee | Up to 0.25% | Up to 0.35% |

| Sales charge | None | None |

Different Financial Year

One thing many people miss - ASB and ASB 2 have different financial years. ASB follows the calendar year (January-December), while ASB 2 ends on 31 March each year. This means ASB dividends are announced in early January, while ASB 2 dividends are usually announced in April.

Dividends

Historically, ASB dividends have been slightly higher than ASB 2. For the most recent year, ASB paid 5.75 sen/unit (FY2025) compared to ASB 2 which paid 5.50 sen/unit (FY2025 ending March 2025).

ASB 2 Dividend History (2015-2025)

Here is the dividend record of ASB 2 since its launch, based on data from ASNB and 1-million-dollar-blog:

| Financial Year | Dividend (sen/unit) | Bonus (sen/unit) | Total (sen/unit) |

|---|---|---|---|

| FY2025 (Apr 2024 - Mar 2025) | 4.75 | 0.75 | 5.50 |

| FY2024 (Apr 2023 - Mar 2024) | 4.25 | 1.00 | 5.25 |

| FY2023 (Apr 2022 - Mar 2023) | 4.25 | 1.00 | 5.25 |

| FY2022 (Apr 2021 - Mar 2022) | 4.60 | 0.50 | 5.10 |

| FY2021 (Apr 2020 - Mar 2021) | 4.25 | 0.75 | 5.00 |

| FY2020 (Apr 2019 - Mar 2020) | 4.25 | 0.75 | 5.00 |

| FY2019 (Apr 2018 - Mar 2019) | 5.00 | 0.50 | 5.50 |

| FY2018 (Apr 2017 - Mar 2018) | 6.50 | 0.50 | 7.00 |

| FY2017 (Apr 2016 - Mar 2017) | 7.00 | 0.25 | 7.25 |

| FY2016 (Apr 2015 - Mar 2016) | 6.75 | 0.50 | 7.25 |

| FY2015 (Apr 2014 - Mar 2015) | 7.25 | 0.50 | 7.75 |

The trend shows a decline in dividends from 7.75 sen (FY2015) to around 5.00-5.50 sen in recent years. However, FY2025 saw an increase to 5.50 sen - the highest rate since FY2019.

For context, the average 12-month fixed deposit (FD) rate at Maybank was around 2.29% in 2025. ASB 2's dividend of 5.50% still far exceeds the FD rate - making it an attractive option for long-term savings.

Advantages of Investing in ASB 2

1. Capital Guaranteed

The fixed unit price of RM1.00 means your capital will not depreciate. You can withdraw at any time and still get back the same amount (or more, if dividends have already been credited).

2. Tax-Exempt Dividends

ASB 2 income distributions are exempt from income tax. Unlike other investments that may be subject to tax, ASB 2 returns go entirely into your pocket.

3. No Sales Charges

You do not need to pay any charges when buying or redeeming ASB 2 units. This means every sen you invest works for you from day one.

4. Additional RM300,000 Capacity

For investors who have already reached the ASB limit, ASB 2 opens an additional RM300,000 in capacity. The combined total of both funds can reach RM600,000 - a significant amount for building long-term wealth.

5. Professional Management by PNB

The fund is managed by professional fund managers at PNB, one of the largest investment management companies in Southeast Asia. You do not need to worry about stock or bond selection - everything is managed by experts.

6. Can Be Used as Collateral

ASB 2 investments can be used as collateral to obtain ASB financing from banks such as Maybank, CIMB, and others.

Disadvantages and Risks of ASB 2

1. Lower Returns Compared to ASB

Consistently, ASB 2 dividends have been slightly lower than the original ASB. If you have not maxed out your ASB limit, it is better to focus on ASB first before moving to ASB 2.

2. Dividends Are Not Guaranteed

Although ASB 2's dividend track record is consistent, the dividend rate is not guaranteed and can change every year depending on market performance. As shown in the table above, dividends have dropped from 7.75 sen to 5.00 sen before.

3. Restricted to Bumiputera Only

Only Malaysian citizens with Bumiputera status are eligible to invest in ASB 2. Non-Bumiputera investors need to look at other ASNB funds such as ASM or ASN.

4. Limited Returns Compared to Stocks

At a rate of 5-6% per year, ASB 2 returns are not as high as the potential stock market returns which can reach 10-15% (or more) per year. However, ASB 2 is far more stable and lower risk.

5. Higher Management Fee

ASB 2's management fee (up to 0.35%) is slightly higher compared to ASB (up to 0.25%). Although the difference is small, it affects long-term net returns.

Who Is Eligible to Invest in ASB 2?

The eligibility to invest in ASB 2 is the same as ASB:

- Malaysian citizens with Bumiputera status

- Aged 18 years and above for individual accounts

- Children aged 6 months to 17 years can open an ASB 2 Youth Account through a guardian

- Eligible Bumiputera institutions

Documents required:

- Original and copy of MyKad (identity card)

- Minimum deposit of RM1 (yes, as low as one ringgit!)

How to Open an Account and Start Investing in ASB 2

Method 1: Online via myASNB

- Visit the myASNB website or download the myASNB app

- Register for a myASNB account if you do not have one yet

- Log in and select "Add Fund" > "ASB 2"

- Enter your investment amount and confirm the transaction

- Payment can be made via internet banking (FPX)

Method 2: At ASNB Counters or Agent Banks

- Visit any ASNB branch or agent bank (Maybank, CIMB, RHB, BSN, AmBank, Bank Muamalat)

- Bring your original MyKad and a copy

- Fill in the account opening form

- Make a minimum deposit of RM1

Method 3: Via Salary Deduction

You can also choose to make automatic investments through monthly salary deductions. Contact your company's HR department for more information.

Strategies to Maximize ASB 2 Returns

1. Max Out ASB First

Since ASB dividends are usually higher, make sure you have already reached the RM300,000 limit in ASB before starting to invest in ASB 2. Once ASB is full, then redirect your investments to ASB 2.

2. Invest Early in the Financial Year

ASB 2's financial year begins on 1 April. Try to put in your investment as early as possible after dividends are credited (usually early April) so your money works throughout the entire financial year.

3. Use Automatic Salary Deductions

Set up automatic monthly salary deductions to your ASB 2 account. This "dollar-cost averaging" method helps you invest consistently without having to remember to make manual transactions.

4. Do Not Withdraw Dividends

Let your dividends be reinvested to take advantage of the power of compound interest. With a 5.50% dividend, an investment of RM300,000 can grow to over RM500,000 within 10 years through the power of compounding alone.

5. Consider ASB 2 Financing

Banks such as Maybank and CIMB offer ASB 2 financing. This allows you to borrow to invest in ASB 2, with the expectation that dividends received will exceed the financing cost. However, this strategy carries its own risks - make sure you fully understand the terms before applying.

Frequently Asked Questions (FAQ) About ASB 2

Is ASB 2 the same as ASB?

No. Although both are managed by ASNB with a fixed unit price of RM1.00, they are two separate funds. ASB 2 uses a mixed-asset strategy while ASB focuses on equities. Each has an investment limit of RM300,000, making the combined total RM600,000.

Can I open ASB 2 without having an ASB account?

Yes. You can open an ASB 2 account without needing to have an ASB account first. However, strategically, it is better to max out ASB first since its dividends are usually higher.

When are ASB 2 dividends credited?

ASB 2 dividends are usually credited on 1 April each year, after the financial year ends on 31 March. This is different from ASB, which is credited on 1 January.

What is the minimum investment for ASB 2?

The minimum investment to open an ASB 2 account is as low as RM1. For subsequent top-ups, the minimum is also RM1 via myASNB.

Can I withdraw money from ASB 2 at any time?

Yes. ASB 2 has high liquidity - you can redeem units at any time without any penalty. The money will be credited to your bank account within a few business days.

Is ASB 2 Shariah compliant?

ASB 2, like ASB, is managed by ASNB/PNB. PNB's Shariah Advisory Council Committee oversees the fund's operations. However, its Shariah compliance status has been a topic of discussion among scholars. The National Fatwa Committee Muzakarah has ruled that investment in ASB funds is harus (permissible).

Can I use EPF money to invest in ASB 2?

Yes. ASB 2 is among the funds approved under the EPF Members' Investment Scheme (EPF-MIS). You can use your EPF Account 1 savings to invest in ASB 2, subject to the terms and limits set by EPF.

How does ASB 2 compare to fixed deposits (FD)?

With a dividend of 5.50 sen/unit (FY2025), ASB 2 returns far exceed the average fixed deposit rate of around 2.29%. Furthermore, ASB 2 dividends are exempt from income tax, making the actual returns even higher.

Conclusion

ASB 2 is a smart investment choice for Bumiputera investors who want to diversify their savings beyond the original ASB. With consistent dividend returns exceeding 5%, guaranteed capital, and professional management by PNB, it remains one of the most attractive savings vehicles in Malaysia.

If you have already maximized your ASB limit and want to continue building wealth, ASB 2 is the logical next step. For those just starting out, focus on ASB first, then expand to ASB 2 once the limit has been reached.

Interested in expanding your investments into the stock market? Open a CDS trading account to start investing in Bursa Malaysia as well as international stocks such as US and Hong Kong.

Want to learn the basics of stock investing from A to Z? Get our Free Stock Market Basics Ebook as your first step.